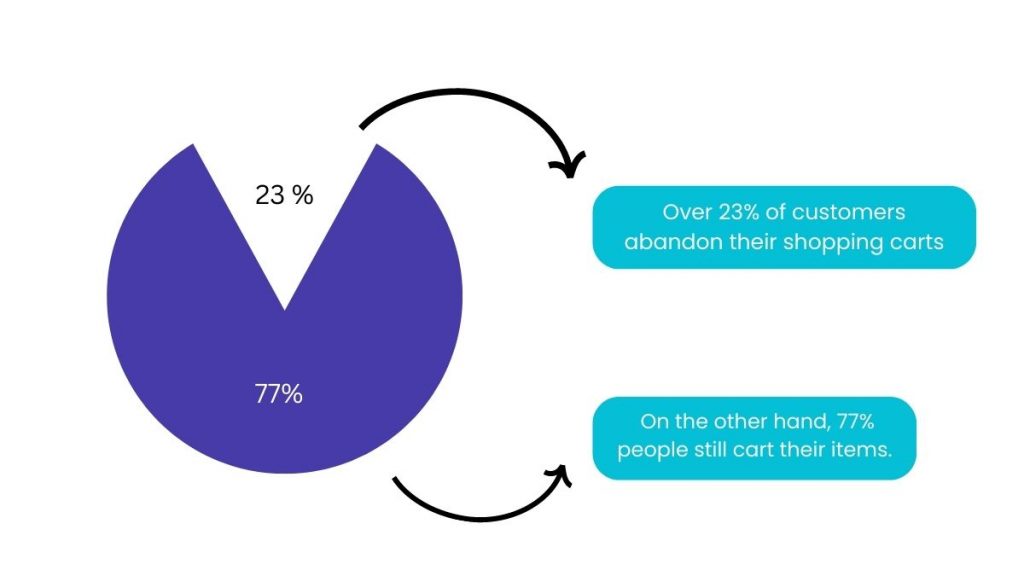

Over 23% of customers abandon their shopping carts, stats say, because the checkout process is either complicated or requires too much information. These figures demonstrate that picking the best payment solution provider is just as crucial to a successful eCommerce business as other factors. But before choosing a payment solution, we must first comprehend what an online payment gateway is and how it operates. And that is exactly what we are going to do in the blog, so keep scrolling!

It doesn’t matter if you run an eCommerce platform or are just keeping up with your online presence—you want to give your consumers a secure, quick, and simple way to pay. The payment method you use must meet the needs of both your customers and your company. Therefore, it must be secure from fraud, accept a range of payment options, be user-friendly, and work with your platform.

A merchant uses a payment gateway to be able to process credit or debit cards and accept electronic payments. The currencies you can accept, the transaction cost, how quickly money enters your merchant account, and the payment options you’ll provide are all impacted by the payment gateway you choose.

But Wait, What is an Online Payment Gateway?

An online and offline merchant can authorize and process payments through a payment gateway. A gateway acts as a doorway to improve the flow of transactions between customers and retailers. Encryption and security procedures are used to transmit transaction data securely. Data is sent back and forth between websites, applications, mobile devices, payment processors, mobile devices, and payment processors, and banks.

The following transaction types can be carried out using payment gateways:

- Authorization transaction: determines if a consumer has sufficient funds to make a purchase. It excludes the actual transfer of funds. Instead, a merchant confirms during an authorization that a cardholder is able to pay for an ordered item. When manufacturing or shipping orders take a while, an authorization transaction is used.

- Captured: A previously allowed payment is “captured” when it is actually processed and money is transferred to the merchant’s account.

- Sale: a mix of capture and authorization transactions. First, a cardholder is authorized. Then, money might or might not be taken. It is a standard method of payment for instant purchases like subscriptions or e-tickets.

- Refund: The outcome of order cancellation, for which a merchant must use a refund payment processing to return the money.

- Void: Similar to a refund, but only possible if the money has not yet been collected.

Online Payment Gateway Integration

The two main strategies that will determine your integration process for an online payment gateway are:

- The degree of user experience regarding the checkout and payment process and

- whether you must adhere to any financial regulations (PCI DSS)

When do you require PCI DSS compliance and what is it?

You can skip this part if all you need is a payment gateway and don’t intend to store or process credit card information. This is because your gateway or payment service provider will take care of all the processing and compliance requirements.

However, you’ll need to adhere to specific industry laws if you’re going to work with sensitive financial data. Processing card payments require the Payment Card Industry Data Security Standard (PCI DSS). The four largest card associations—Visa, MasterCard, American Express, and Discover—created this security standard in 2004.

You must fulfill the following 5 stages to become PCI compliant:

- Set your degree of compliance. The number of secure transactions your company has completed will determine which of four compliance tiers your company falls under. If a particular amount of transactions were successfully completed and they were made using a MasterCard, Visa, American Express, or Discover card, the transaction counts.

- Learn more about the PCI Self-Assessment Questionnaire (SAQ). SAQ consists of a number of requirements and prerequisites. The most recent version has 12 prerequisites.

- Submit the Attestation of Compliance in full (AOC). After reviewing the prerequisites, you take an exam of this type called an AOC. There are nine different AOC kinds for various business types. AOC SAQ D – Merchants are the ones needed by retailers.

- Perform an external vulnerability scan with the authorized scanning vendor (ASV).

- Send your documentation to the acquiring bank and card associations. The ASV scan report as well as your completed SAQ and AOC are among the documents.

With this knowledge, we’ll explore the available online payment gateway integration choices and list their advantages and disadvantages.

Hosted gateway

A hosted online payment gateway takes on the role of an outsider. Therefore, in order to make a purchase, your customers must exit your website. In essence, a consumer is routed to a payment gateway web page to enter their credit card number in that situation. The customer is directed back to the merchant’s page after the transaction data has been sent. Here, the checkout is completed and the transaction approval is displayed.

This mode of payment is more suitable for small businesses that are comfortable with external payment processors.

The benefit of a hosted payment gateway is that the service provider handles all aspects of payment processing. The seller also retains customer credit card information. Therefore, employing a hosted gateway allows rather simple integration and does not require PCI compliance.

The absence of control over a hosted gateway is one of the drawbacks. Customers might not have faith in third-party payment methods. Additionally, diverting visitors away from your website reduces conversion rates and hurts your branding.

How to integrate: The vendor’s websites often have open integration guides, and the connection is made via an API. As an illustration, PayPal Checkout recommends integration using a Smart Payment Button. It’s essentially a line of HTML code that adds a PayPal button to your checkout page. Every time a user presses the button, it contacts the PayPal REST API to validate, gather, and submit payment information through a gateway.

Direct Post

Since you don’t need to achieve PCI compliance, Direct Post is an integration solution that enables a customer to shop without leaving your website. After a customer clicks the “buy” button, Direct Post anticipates that the transaction’s data will be posted to the payment gateway. Without being kept on your server, the data is sent directly to the gateway and processor.

The benefits of this approach are comparable to those of an integrated payment gateway. Without PCI DSS compliance, you still have branding and personalization possibilities. All required actions are completed by the user on a single page.

The drawback of using Direct Post, however, is that it’s not 100 percent secure.

How to integrate: To publish the card data, a vendor would put up an API connection between your shopping cart and its payment gateway.

Integrated (non-hosted) technique

A payment gateway that is integrated basically indicates that there are no outside parties engaged throughout the payment checkout process. Companies that use integrated gateways achieve PCI DSS compliance, which implies they are in charge of keeping each transaction secure and doing the initial transaction verification. Installing a payment gateway program from the merchant’s website accomplishes this.

White-label payment gateways can occasionally be used by businesses as a non-hosted alternative. Essentially, this is a prebuilt gateway that can be altered and branded with your logo.

With merchants becoming their own payment service providers when they achieve essential compliance, an integrated online payment gateway can be a dedicated source of income. This indicates that for a fee, your company can accept payments for other retailers. Being a provider of payment gateways has a technological cost in addition to the regulatory one because you require an infrastructure to securely store transaction data, credit card tokens, etc.

The advantage is that you are in complete control of website transactions. Your payment system can be modified to suit your preferences and needs as a business. A white-label solution uses your branded technology as the payment gateway.

The drawbacks often revolve around the upkeep of your payment system’s infrastructure and associated costs. You must first be PCI compliant in order to use an integrated gateway because you will need to store all client credit card information on your own servers. Also, if you wish to provide customized features, integrating the gateway can be challenging.

Non-hosted payment gateways are included in your server through APIs. Consequently, the integration will need to be done by an engineering team. The majority of vendors have developer portals, API references, and integration guidelines that are well-documented.

How to Choose an Online Payment Gateway Provider?

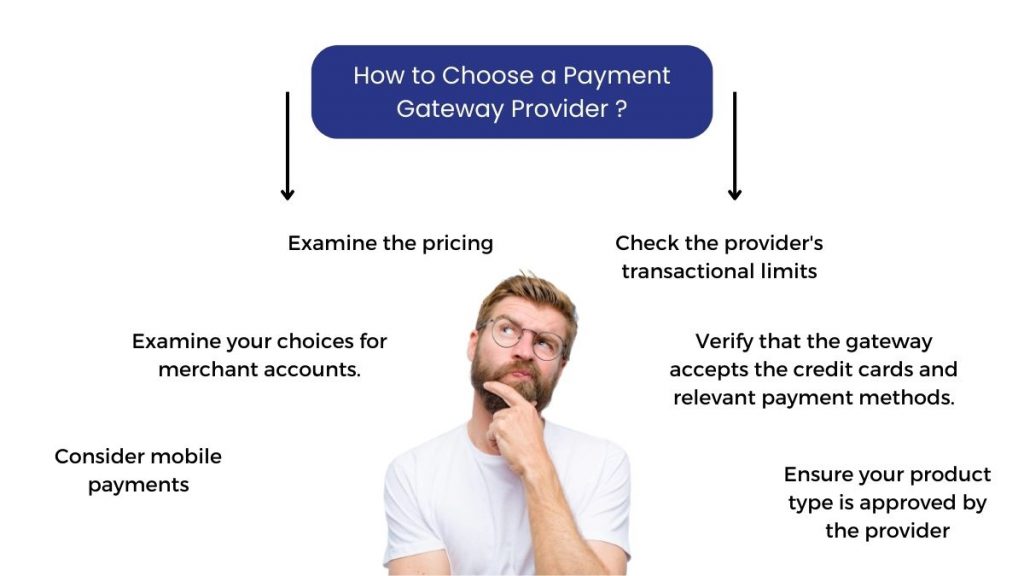

You can now select a payment option for your company while taking all relevant criteria, your company’s unique circumstances, and your clients into account. Here are a few things to think about before choosing a supplier.

Examine the pricing

Payment processing is often complicated due to the involvement of numerous financial institutions or organizations. A payment gateway charges a fee for using third-party technologies to complete and authorize the transaction, just like any other service. Every party involved in the verification, authorization, or processing of payments levies fees. Transactions are frequently charged based on the sum, location (inside a country or internationally), and category of a product (physical or digital).

Each provider of payment solutions has its own usage guidelines and costs. The following fee kinds are typically included: setup fees for your merchant account, monthly gateway fees, setup fees for your gateway, and fees for each transaction that is performed.

Check the provider’s transactional limits.

Even while fees and installation costs are unavoidable, there is one factor that could affect your ability to cooperate with a particular provider. Gateway providers establish minimum and maximum transaction limits. Since you want to use a single gateway for all of the accessible products, these values are important to merchants and their businesses.

You should pay attention to any daily or monthly transaction limits. These are comparatively rare but also have a significant impact on the choice of a gateway provider.

Examine your choices for merchant accounts.

In exchange for allowing a bank to handle their transactions, a merchant and an acquiring bank enter into a merchant account arrangement. A merchant also consents to abide by the operational guidelines for credit card processing set out by credit card firms.

Banks and payment gateway providers that provide merchant accounts as a service can be used to open one. Processors of payments are included below. Think over the options offered by your current merchant supplier if you currently have one. Otherwise, it’s preferable to pick a service provider who provides a merchant account right away.

Verify that the gateway accepts the credit cards and relevant payment methods.

According to Statista, the most common payment method for all consumers as of 2019 ranges from 82 to 69 percent using credit cards. With between 51 and 80 percent of all transactions, several electronic payment systems including PayPal, Union Pay, and Alipay come in second.

You need to confirm that a payment gateway accepts the necessary credit card networks if you plan to use credit cards as a primary form of payment.

Support for many currencies is another factor. If your company conducts business internationally, you want your clients to be able to make payments in whichever currency they want. Several well-known gateway providers provide multi-currency support processing, either for free or at a cost. Additional localized checkouts are accessible if you plan to use a hosted payment system.

Consider mobile payments

Accepting Apple Pay or Google Pay necessitates providing a distinct payment method even when mobile payments are drawing funds from credit card accounts. In fact, mobile payments arrive as a different method in all payment gateway providers and have their own tokenization procedure.

Mobile wallets may or may not be available in the nation where you conduct business. However, the three most popular apps—Apple Pay, Google Pay, and Samsung Pay—are available in hundreds of nations and currently support all four major credit card networks. In order to determine which mobile wallets the gateway supports and whether it does, you must search the provider’s website.

Ensure that your product type is approved by the provider

Digital and physical products are typically the two categories that suppliers take into account.

Some companies that offer payment solutions provide both services for physical and digital goods. However, it’s not unusual for a system to exclusively support one kind of product. Therefore, check to see if a supplier allows your type of goods before subscribing.

Conclusion

Therefore, unless you run a non-profit website, it is always a lot better for an online merchant to choose a payment gateway/processor provider or to prepare to develop your own payment portal. Websites employing an incorporated online payment gateway method are more trusted by customers. Incorporate a payment solution that will inspire trust, enable different payment ways, and be secure if you’re searching for a means to increase customer confidence.

One great way to integrate a personalized payment portal for your business is by taking your business to Exly.

Creators get a pool of professional tools and exposure when they become an #Exlypreneur. So, what are you waiting for? Try out all the cool features now and your business will thank you!